Best Mortgage Rates in Ireland - April 2024

Best mortgage rates in Ireland is essentially the lowest interest rate and/or APRC (annual percentage rate of change). However getting a mortgage to buy a home is one of the biggest purchase most people will ever make. The mortgage rate you choose can make thousands of euros worth of difference to your long-term costs. In this article you will find the best mortgage rates for first time buyers, home mover, switchers or remortgagers. In addition find out out what to look out for when comparing mortgages.

We have compiled these resources without taking into account your personal objectives, circumstances, financial situation or needs. Therefore, before acting on any information contained on this website you should consider the appropriateness of the information having regard to your objectives, financial situation and needs, and seek professional advice where appropriate. You can read the full Terms of Use.

Irish Mortgage Rates

Interest rates determine the costs of borrowing to start or develop a business, or to buy a house or a car, or personal loans, loans to fund a health service or education system. It determine how much money that’s saved on deposit will earn. Interest rates can vary depending on the purpose of a loan, the time needed to repay the loan, and the risk that the loan represents to the lender, among other things.

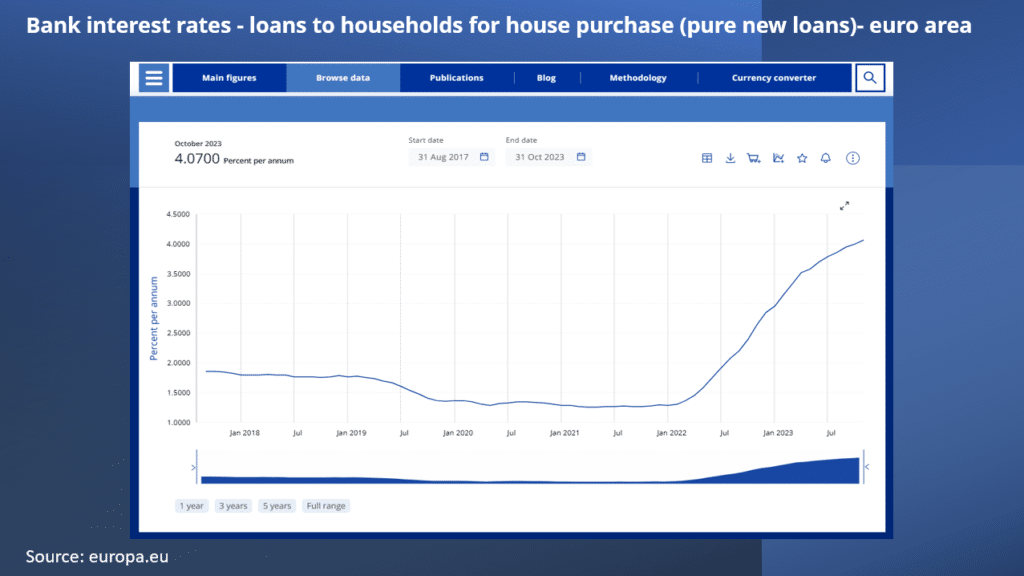

The European central bank sets the key interest rates that banks pay when they borrow money from ECB or receive money from ECB. These interest rates impacts the Irish economy via banking system because the rate set by ECB influences the interest rate commercial banks in Ireland charge their customers including mortgages customers. The average Irish mortgage rates is now well above 4%, which is the highest level in about 10 years. This huge jump in rates in June 2023 caused a big squeeze on disposable income of mortgage holders. Getting the best mortgage rate can mean a lot of savings for your budget.

>> Read More: Check out interest rates on personal loans in Ireland and Check out interest rates on Credit Cards

We will be reviewing the below types of mortgage rates.

- Best First Time Buyer Mortgage in Ireland

- Best Fixed Rate Mortgage in Ireland

- Best Buy to Let Mortgage Deals in Ireland

- Best Green Mortgage Deals in Ireland

Best First Time Buyers Mortgage Deals in Ireland

A good step for someone looking to get on the property ladder is to speak to a mortgage adviser. First time buyers typically want to put down a lower deposit which means that they find a high loan to value attractive. As a first time buyer in Ireland, you might be eligible for help to buy schemes or first home scheme programs to help get on the property ladder. Most mortgage lenders in Ireland offer separate interest rates for first time buyers. As a first time buyer, a fixed rate mortgage is easier and more straightforward. In the table below we listed the best first time buyer fixed mortgage rate deals for LTV > 80% for a mortgage lower than €250,000.00 for 25 years.

Best 1-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

EBS |

90% LTV Max |

4.55% |

4.3% |

|

Haven Mortgages |

90% LTV Max |

4.55% |

4.3% |

|

Bank of Ireland |

>80% LTV |

4.65% |

4.9% |

Best 2-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

Haven Mortgages |

90% LTV Max |

4.65% |

4.4% |

|

Bank of Ireland |

90% LTV Max |

4.65% |

4.9% |

|

AIB |

>80% LTV |

4.70% |

4.37% |

Best 3-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

Avant Money |

80% -90% |

4.05% |

4.08% |

|

Haven Mortgages |

90% LTV Max |

4.75% |

4.5% |

|

Bank of Ireland |

>80% |

4.75% |

4.9% |

|

AIB |

>80% |

4.80% |

4.46% |

Best 4-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

Avant Money |

80% – 90% |

4.10% |

4.11% |

|

PTSB |

>80% |

4.75% |

4.62% |

|

AIB |

>80% |

4.85% |

4.54% |

Best 5-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

Avant Money |

80% – 90% |

4.10% |

4.12% |

|

Bank of Ireland |

>80% |

4.75% |

4.9% |

|

Haven Mortgages |

90% LTV Max |

4.85% |

4.6% |

Best 7-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

Avant Money |

80% – 90% |

4.10% |

4.14% |

|

Haven Mortgages |

90% LTV Max |

5.05% |

4.9% |

|

AIB |

>80% |

5.15% |

4.9% |

Best 10-year fixed rate mortgage deals for first time buyers

| Mortgage Lender | Loan to Value | Interest Rate | Indicative APRC |

|---|---|---|---|

|

Avant Money |

80% – 90% |

4.10% |

4.17% |

|

Haven Mortgages |

90% LTV Max |

5.15% |

5% |

|

Bank of Ireland |

>80% |

5.25% |

5.4% |

|

AIB |

>80% |

5.30% |

5.2% |

Read more >> Best first time buyer mortgage deals in Ireland

Best Fixed Rate Mortgage Deals in Ireland

Existing homeowners who don’t plan on moving homes for a long time might want to consider fixed rate mortgages to avoid future unexpected rises in interest rates. Home movers, switchers and remortgagers, generally prefer fixed rate mortgages if they are people who like to set budget and need to know how much to set aside for a mortgage payment. In the tables below , we will show best mortgage rates for 2-year, 3-year, 4-year, 5-year, 7-year and 10-years. The rates are based on ≤60%, 61% – 80% and >80% for a mortgage of €250,000 over 25years.

Best 2-year fixed rate mortgage deals - Existing home owners

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Existing only |

≤60% |

4.15%

|

4.30% |

|

Bank of Ireland |

Existing only |

61%-80% |

4.15% |

4.30% |

|

Bank of Ireland |

Existing only |

>80%

|

4.15%

|

4.70% |

|

AIB |

Existing, home mover & switcher |

≤50% |

4.45%

|

3.99% |

|

AIB |

Existing, home mover & switcher |

51%-80% |

4.60%

|

4.19% |

|

AIB |

Existing, home mover and switcher |

>80%

|

4.70%

|

4.37%

|

Best 3-year fixed rate mortgage deals - Existing home owner

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Existing only |

≤60%

|

4.25%

|

4.40% |

|

Bank of Ireland |

Existing only |

61%-80%

|

4.25% |

4.40% |

|

Bank of Ireland |

Existing only |

>80%

|

4.25% |

4.70% |

|

AIB |

Existing, home mover & switcher |

≤50%

|

4.55%

|

4.09% |

|

PTSB |

Existing, home mover & switcher |

61%-80%

|

4.65% |

4.21% |

|

AIB |

Existing, home mover & switcher |

>80%

|

4.80% |

4.46% |

Best 4-year fixed rate mortgage deals - Existing home owner

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Home mover & switcher |

≤60%

|

3.95%

|

4.20% |

|

Bank of Ireland |

Home mover & switcher |

61% – 80%

|

3.95%

|

4.40% |

|

Bank of Ireland |

Home mover & switcher |

>80%

|

3.95%

|

4.40% |

Best 5-year fixed rate mortgage deals - Existing home owner

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Existing, home mover & switcher |

≤60%

|

4.25%

|

4.40% |

|

Bank of Ireland |

Existing, home mover & switcher |

61% – 80%

|

4.25%

|

4.50% |

|

Bank of Ireland |

Existing, home mover & switcher |

>80%

|

4.25%

|

4.60% |

Best 7-year fixed rate mortgage deals - Existing home owner

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Existing, home mover & switcher |

≤60%

|

4.30%

|

4.40% |

|

Bank of Ireland |

Existing, home mover & switcher |

61% – 80%

|

4.30%

|

4.50% |

|

Bank of Ireland |

Existing, home mover & switcher |

>80%

|

4.30%

|

4.60% |

Best 10-year fixed rate mortgage deals - Existing home owner

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Existing only |

≤60% |

4.55%

|

4.70% |

|

AIB |

Existing, home mover & switcher |

≤50% |

5.05%

|

4.90% |

|

Bank of Ireland |

Existing only |

61%-80% |

4.55% |

4.70% |

|

AIB |

Existing, home mover & switcher |

51%-80% |

5.20%

|

5.07% |

|

Bank of Ireland |

Existing only |

>80%

|

4.75%

|

4.90% |

|

AIB |

Existing, home mover and switcher |

>80%

|

5.30%

|

5.20%

|

Best Green Mortgage Deals in Ireland

Green mortgages are available to new and existing home loan customers looking to buy, build, structurally renovating or currently own a high energy rated home. Existing customers who own a home or looking to have a building energy rating of A1 to B3 (inclusive), and you have 5 years remaining on your mortgage term, you may be able to get a Green rate mortgage. The table below shows the best green mortgage rate on a mortgage of €250,000 over 25 years.

Best 4-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

All – Including First time buyers |

≤60%

|

3.65%

|

4% |

|

Bank of Ireland |

All – Including First time buyers |

61% – 80%

|

3.65%

|

4.20% |

|

Bank of Ireland |

All – Including First time buyers |

>80%

|

3.65%

|

4.40% |

Best 5-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

AIB |

All – Including First time buyers |

≤50%

|

3.65%

|

3.79% |

|

AIB |

All – Including First time buyers |

51% – 80%

|

3.75%

|

3.96% |

|

AIB |

All – Including First time buyers |

>80%

|

3.85%

|

4.12% |

Best 7-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

All – Including First time buyers |

≤60%

|

4%

|

4.20% |

|

Bank of Ireland |

All – Including First time buyers |

61% – 80%

|

4%

|

4.30% |

|

Bank of Ireland |

All – Including First time buyers |

>80%

|

4%

|

4.40% |

Best Buy to Let Mortgage Deals in Ireland

If you are thinking of investing in real estate and becoming a landlord, a buy to let mortgage is available for get on the property investment ladder. Landlords also need to consider buy to let interest rate and the cost of the mortgage and compare against potential rental income, to measure the profitability of the investment. The interest rate on buy to let are higher than interest rate for residential properties because of the risk involved if tenant don’t pay their rent. Also to consider is the minimum LTV for a buy to let are usually higher than the residential. properties. Below table shows the best buy to let rate for a mortgage.

Best 2-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

Bank of Ireland |

Green Mortgage |

<50%

|

6.20%

|

6.60% |

|

Bank of Ireland |

New Investor |

<50%

|

6.50%

|

6.90% |

|

Bank of Ireland |

Existing investor |

<50%

|

6%

|

6.40% |

|

Bank of Ireland |

Existing Investor |

50% – 75%

|

6.24%

|

6.60% |

|

Bank of Ireland |

Green Mortgage |

50% – 75%

|

6.44%

|

6.80% |

|

Bank of Ireland |

New Investor |

50% – 75%

|

6.74%

|

7.10% |

Best 3-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

PTSB |

All – Including First time buyers |

≤70%

|

5.65%

|

5.93% |

|

AIB |

All – Including First time buyers |

50%-75%

|

7.70%

|

n/a |

Best 4-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

AIB |

All – Including First time buyers |

50%-75%

|

7.90%

|

n/a |

Best 5-year fixed rate mortgage deals

| Mortgage Lender | Customer Type | LTV | Interest Rate | APRC |

|---|---|---|---|---|

|

PTSB |

All – including first time investor |

≤70%

|

5.85%

|

6.06% |

|

Bank of Ireland |

Existing investor |

<50%

|

6.15%

|

6.50% |

|

Bank of Ireland |

Green Mortgage |

<50%

|

6.35%

|

6.70% |

|

Bank of Ireland |

New Investor |

<50%

|

6.65%

|

7% |

|

Bank of Ireland |

Existing Investor |

50% – 75%

|

6.35%

|

6.70% |

|

Bank of Ireland |

Green Mortgage |

50% – 75%

|

6.55%

|

6.90% |

|

Bank of Ireland |

New Investor |

50% – 75%

|

6.85%

|

7.30% |

How are mortgage rates determined in Ireland?

There are several factors that determine the mortgage interest rate that a bank charges for your home. Find below a list of some of these from the Central bank of Ireland

- Economic factors and monetary policies: Interest rates are a core part of the monetary policy and it determine the costs of borrowing to start or develop a business, or to buy a house or a car, or to fund a health service or education system. In detail these are the main issues that affect monetary policies and interest rates.

- The cost of funding: Banks’ funding can come from a range of sources such as customer deposits and wholesale markets and from central banks. The mix of this funding is influenced by regulatory requirements. For new lending, banks consider the cost of raising new funding, usually with some reference to interest rates in the market (and often reflecting their funding mix and the interest rates on deposits to customers).

- Credit risk: Banks must also take into account the riskiness of their lending when setting interest rates as they need to consider that some borrowers may find themselves unable to pay back their loan.

- Operating costs: The costs of developing, distributing and managing the loan and the customer relationship also needs to be captured as part of the bank’s assessment of the appropriate rate to charge on new lending. (In the first half of this year the underlying cost to income ratio of the three quoted Irish banks was 76% compared 65% for a range of EU and UK peers)

- Cost of capital: The amount of capital that banks fund themselves with varies from bank to bank and depends on factors such as a bank’s business model, how risky a bank’s assets are or have been and other considerations on risk profile.6 And of course equity funding costs as investors expect a return on their investment

Read More>> How mortgage rates are determined

Personal Factors that affect the cost of your mortgage?

- Purpose of the mortgage: is the house a PDH – primary dwelling residence or buy to let property? the purpose of the property determines the mortgage rate.

- Loan to value: The amount of deposit that you put down on the property will affect the mortgage rate applied to your loan.

- Credit history: Your personal credit history determines if the mortgage will be approved and the your credit profile will evaluate risk.

Read more>> How to manage your mortgage?

Types of mortgage interest rates

There are three types of mortgage interest rate:

- Fixed rate mortgage: This type of mortgage rate is fixed which means that the monthly mortgage payment you make is fixed and agreed for future point. It is simple and convenient for those who like a set budget.

- Variable rate mortgage: This type of interest rate moves at the discretion of the lender. In many cases, differentiated Variable rates are applied by the same lender at different levels of Loan toValue (LTV).

- Tracker mortgage: This type of interest rate moves mechanically in line with a reference rate such as the ECB’s Main Refinancing Operation rate. It tracks the ECB rates.

Read more>> Understanding the different type of mortgages

Find Mortgage Calculators of Top Mortgage Lenders

To better understand your affordability and readiness for a mortgage, a mortgage calculator will help you estimate how much you can borrow based on your deposit, interest rates and length of mortgage loan.

If you are already a home owner with a mortgage and looking to switch, remortgage or move homes or make overpayments, mortgage calculator can work out these payments for you. Here are some of the mortgage calculators, top Irish mortgage lenders have available.

PTSB Mortgage Calculator

EBS Mortgage Calculator

Mortgage Rates FAQ

What are APRC's?

Assuming that you will keep the mortgage for the full term, APRC - Annual percentage rate of change is the total cost of the mortgage per year and includes fees and charges over the full term of the mortgage. When comparing mortgages it is also good practise to compare the APRC of the loan and CCPC also recommends using the APRC to compare morgages.

Types of mortgage buyers?

There are 3 different types of home buyers in the UK

- First time buyers

- Home movers

- Switchers/remortgagers

Why you should use a mortgage broker?

Here are the benefits of using a mortgage adviser or broker to guide you in your home buying process instead of direct application.

- Mortgage brokers have better knowledge of the lenders and closer relationship with lenders. Based on your circumstances, they know which lenders which you may have a higher probability of success.

- Mortgage brokers will complete your application and screen your application, reviewing and addressing blind spots which lenders will query.

- Generally using a mortgage broker saves you time and effort in mortgage research process.

How to find the best mortgage deal?

To be prepared and get the best mortgage deal:

- Clean up your financial profile

- Start saving early for a large deposit

- Take advantage of the help to buy scheme for first time buyers

- Research different mortgage lenders.

- When you are ready consider using a mortgage broker

How long should you fix your mortgage for?

Due to the facts that interest rates are unpredictable and best to reduce this risk by fixing the rates, however the length of the fixed interest really depends on your personal circumstances, personal risks, preference and your budget.

Read more>> How long should you fix your mortgage rate for?

How do I find our my Property Value?

To estimate the value of your property and help you understand the value of similar houses sold recently, you can go and check the property price register.

Mortgage rates by length of loan

1-year fixed rate mortgage rates

2-year fixed rate mortgage rates

3-year fixed rate mortgage rates

4-year fixed rate mortgage rates

5-year fixed rate mortgage rates

7-year fixed mortgage rates

10-year fixed mortgage rates

15- year fixed mortgage rates

20-year fixed mortgage rates

25-year fixed mortgage rates

30-year fixed mortgage rates

Mortgage Arrears - What You Should Do?

If you are struggling to make your mortgage repayments or are in arrears. You need to first contact your mortgage lender to discuss what options that can be available to you. The Central Bank has a statutory Code of Conduct on Mortgage Arrears (CCMA) to help you if you are already or facing difficulty paying you mortgage. Regulated banks and mortgage lenders must follow these guidelines should your account fall into arrears. The code was set out to ensure that lenders work with you to get you back on top of your mortgage repayments.

Lynda Unogu MBA IMC (CFA UK) PMP

Lynda holds an MBA from University College Dublin and worked previously in product roles within financial services and technology firms like Mastercard, Citi Bank and JP Morgan. She constantly seeks to apply her expertise in financial services to the field of personal finance with the goal of helping people navigate the complexities of the finance.